BEIS guidance on Restart Grants published

The Restart Grant scheme supports businesses in reopening safely as COVID-19 restrictions are lifted. Grants will be available from 1 April 2021 but you can submit applications in advance.

Eligible businesses in the non-essential retail sector (including charity shops) may be entitled to a one-off cash grant of up to £6,000 from their local council. Eligible businesses in the hospitality, accommodation, leisure, personal care and gym sectors may be entitled to a one-off cash grant of up to £18,000 from their local council. For charities this includes scout huts, village halls, botanical gardens, attractions, zoos, concert halls, museums and galleries.

Your business may be eligible if it is:

- based in England

- rate-paying

- in the non-essential retail, hospitality, accommodation, leisure, personal care or gym sectors

- trading on 1 April 2021

You cannot get funding if your business:

- is in administration, insolvent or has been struck off the Companies House register

- has exceeded the permitted subsidy allowance

You must notify your local council if your situation changes and you no longer meet the eligibility criteria.

This scheme is covered by 3 subsidy allowances:

- Small Amounts of Financial Assistance Allowance – you’re allowed up to £335,000 (subject to exchange rates) over any period of 3 years

- COVID-19 Business Grant Allowance – you’re allowed up to £1,600,000

- COVID-19 Business Grant Special Allowance – if you have reached your limits under the Small Amounts of Financial Assistance Allowance and COVID-19 Business Grant Allowance, you may be able to access a further allowance of funding under these scheme rules of up to £9,000,000, provided certain conditions are met

Grants under these 3 allowances can be combined for a potential total allowance of up to £10,935,000 (subject to exchange rates). Further details about subsidy allowance can be found here.

Visit your local council’s website to find out how to apply:

Detailed guidance (extracts)

How much funding will be provided to businesses?

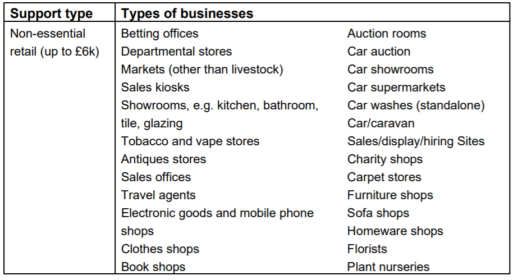

11.The Restart Grant scheme is for businesses on the ratings list only.

12.The Restart Grant is a one-off grant.

13.The Restart Grant will support non-essential retail premises with one-off grants of up to £6,000 in Strand One of the Restart Grant. The following thresholds apply for these businesses:

a. Businesses occupying hereditaments appearing on the local rating list with a rateable value of exactly £15,000 or under on 1 April 2021 will receive a payment of £2,667.

b. Businesses occupying hereditaments appearing on the local rating list with a rateable value over £15,000 and less than £51,000 on 1 April 2021 will receive a payment of £4,000.

c. Businesses occupying hereditaments appearing on the local rating list with a rateable value of exactly £51,000 or over on 1 April 2021 will receive a payment of £6,000.

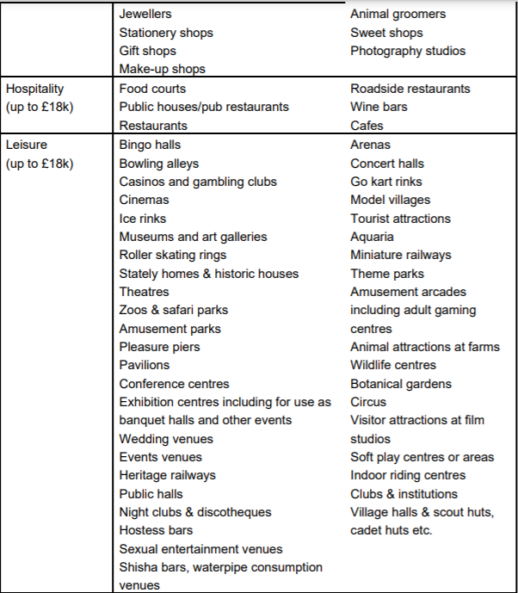

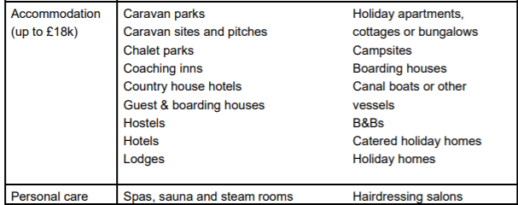

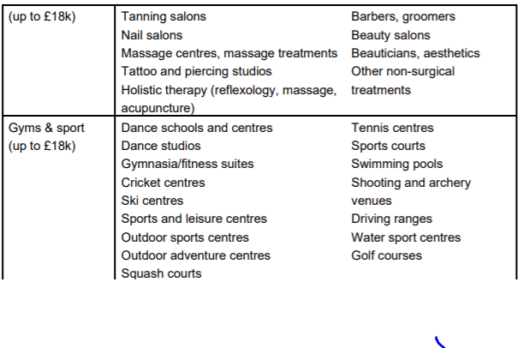

14. The Restart Grant will also support hospitality, accommodation, leisure, personal care and gym business premises with one-off grants of up to £18,000 in Strand Two of the Restart Grant. The following thresholds apply for these businesses:

a. Businesses occupying hereditaments appearing on the local rating list with a rateable value of exactly £15,000 or under on 1 April 2021 will receive a payment of £8,000.

b. Businesses occupying hereditaments appearing on the local rating list with a rateable value over £15,000 and less than £51,000 on 1 April 2021 will receive a payment of £12,000. c. Businesses occupying hereditaments appearing on the local rating list with a rateable value of exactly £51,000 or over on 1 April 2021 will receive a payment of £18,000.

15. Any changes to the rating list (rateable value or to the hereditament) after 1 April 2021 should be ignored for the purposes of eligibility. Local Authorities are not required to adjust, pay or recover grants where the rating list is subsequently

amended retrospectively to 1 April 2021. In cases where it was factually clear to the Local Authority on 1 April 2021 that the rating list was inaccurate on that date, Local Authorities may withhold the grant and/or award the grant based on their view of who would have been entitled to the grant had the list been accurate. This is entirely at the discretion of the Local Authority and only intended to prevent manifest errors.

16.Businesses will be eligible for this support from 1 April 2021 and Local Authorities must not make payments to businesses before this date. Subject to subsidy allowance conditions, businesses will be entitled to receive a grant for each eligible hereditament. So, some businesses may receive more than one grant where they have more than one eligible hereditament.

Who will receive this funding?

General eligibility

17. Where a grant is issued, the business that according to the billing authority’s records was the ratepayer in respect of the hereditament on 1 April 2021 is eligible to receive the grant. Where a Local Authority has reason to believe that the information that they hold about the ratepayer is inaccurate they may withhold or recover the grant and take reasonable steps to identify the correct ratepayer. Local Authorities should make clear to recipients that the grant is for the ratepayer and may be liable for recovery if the recipient was not the ratepayer on the eligible day.

18. Local Authorities will be responsible for determining whether businesses are entitled to a grant under the non-essential retail thresholds, or under the hospitality, accommodation, leisure, personal care and gym business thresholds.

19. The primary principle of the Restart Grant scheme is to support businesses that offer in-person services, where the main service and activity takes place in a fixed rate-paying premises, in the relevant sectors.

20.Annex C gives a list of businesses that fall into scope for each sector. This list is indicative of the types of businesses, but is not exhaustive. Local Authorities will have to use their local knowledge and the definitions and criteria set out below to

assist in making a decision on eligibility of a business for this scheme.

21.If a business operates services that could be considered non-essential and also fall into another category, such as hospitality in the higher funding threshold, the main service can be determined by assessing which category constitutes 50% or more of their overall business. The main service principle will determine which threshold of funding a business receives. Businesses will need to declare which is their main service. Local Authorities will need to exercise their reasonable judgement to determine whether or not a business is eligible for grants under which funding threshold and be satisfied that they have taken reasonable and practicable steps to pay eligible businesses and to pay them the correct amount.

22.It is understood that in some cases it may not be materially clear whether a business falls into one of the categories, so decisions on the eligibility of these businesses will be at the Local Authorities discretion.

23.Businesses must have been trading on 1 April 2021 to be eligible to receive funding under this scheme.

24.For the purposes of this grant scheme, a business is considered to be trading if it is engaged in business activity. This should be interpreted as carrying on a trade or profession, or buying and selling goods or services in order to generate turnover. Fully constituted businesses in liquidation, dissolved, struck off or subject to a striking-off notice are not eligible under these conditions.

25.To help further, some trading indicators are included below that can help assess what can be defined as trading for the purposes of the grant schemes. Indicators that a business is trading are:

- The business has staff on furlough

- The business continues to trade online, via click and collect services etc.

- The business is not in liquidation, dissolved, struck off or subject to a striking of notice or under notice

- The business is engaged in business activity; managing accounts, preparing for reopening, planning and implementing COVID-safe measures

This list of indicators is not exhaustive and Local Authorities must use their

discretion to determine if a business is trading.

26.Local Authorities will need to run an application process for all first-time applicants for a COVID-19 business grant and must be satisfied that businesses that have previously received related grants under this scheme meet the eligibility criteria for the Restart Grant. As a minimum, Local Authorities must hold the following information on all applicants:

a. Name of business

b. Business Trading Address including postcode

c. Unique identifier (preferably Company Reference Number (CRN)) if applicable. If not applicable, VAT Registration Number, SelfAssessment/Partnership Number, National Insurance Number, Unique Taxpayer Reference, Registered Charity Number will also be acceptable)

d. High level SIC Code

e. Nature of Business

f. Date business established

g. Number of employees

h. Business rate account number (if applicable)

i. Cumulative total of previous funding received under all COVID-19 business grants schemes

27.In addition, the application process should also enable Local Authorities to carry out the required pre-grant fraud checks (including unique identifier), as well as the minimum data reporting requirements set out in Annex A.

Strand One: up to £6,000 per hereditament (Non-essential retail)

28. For the purposes of this scheme, a non-essential retail business can be defined as a business that is used mainly or wholly for the purposes of retail sale or hire of goods or services by the public, where the primary purpose of products or services provided are not necessary to the health and well-being of the public.

29. Local Authorities may use the following criteria to assess whether a business is eligible for a grant under this threshold:

- Businesses offering in-person non-essential retail to the general public.

- Businesses that were likely to have been required to cease their retail operation in the January 2021 lockdown.

- Businesses that had retail services restricted during January lockdown.

- Businesses that sell directly to consumers.

30. For these purposes, the definition of a non-essential retail business should exclude: food retailers, including food markets, supermarkets, convenience stores, corners shops, off licences, breweries, pharmacies, chemists, newsagents, animal rescue centres and boarding facilities, building merchants, petrol stations, vehicle repair and MOT services, bicycle shops, taxi and vehicle hire businesses, education providers including tutoring services, banks, building societies and other financial providers, post offices, funeral directors, laundrettes and dry cleaners, medical practices, veterinary surgeries and pet shops, agricultural supply shops, garden centres, storage and distribution facilities, wholesalers, employment agencies and businesses, office buildings, automatic car washes and mobility support shops.

Strand Two: up to £18,000 per hereditament (Hospitality)

31.For the purposes of this scheme, a hospitality business can be defined as a business whose main function is to provide a venue for the consumption and sale of food and drink.

32.Local Authorities may use the following criteria to assess whether a business is eligible for a grant under this threshold:

- Businesses offering in-person food and drink services to the general public.

- Businesses that provide food and/or drink to be consumed on the premises, including outdoors.

33.For these purposes, the definition of a hospitality retail business should exclude: food kiosks and businesses whose main service is a takeaway (not applicable to those that have adapted to offer takeaways during periods of restrictions, in alignment with previous COVID-19 business grant schemes).

Leisure

34.For the purposes of this scheme, a leisure business can be defined as a business that provides opportunities, experiences and facilities, in particular for culture, recreation, entertainment, celebratory events and days and nights out .

35.Local Authorities may use the following criteria to assess whether a business is eligible for a grant under this threshold:

- Businesses that may provide in-person intangible experiences in addition to goods.

- Businesses that may rely on seasonal labour.

- Businesses that may assume particular public safety responsibilities.

- Businesses that may operate with irregular hours through day, night and weekends.

36.For these purposes, the definition of a leisure business should exclude: all retail businesses, coach tour operators, tour operators and telescopes.

Accommodation

37.For the purposes of this scheme, an accommodation business can be defined as a business whose main lodging provision is used for holiday, travel and other purposes.

38.Local Authorities may use the following criteria to assess whether a business is eligible for a grant under this threshold:

- Businesses that provide accommodation for ‘away from home’ stays for work or leisure purposes.

- Businesses that provide accommodation for short-term leisure and holiday purposes.

39.For these purposes, the definition of an accommodation business should exclude: private dwellings, education accommodation, residential homes, care homes, residential family centres, beach huts.

Gym & sports

40. For the purposes of this scheme, a gym & sport business can be defined as a commercial or non-profit establishment where physical exercise or training is conducted on an individual basis or group basis, using exercise equipment or open floor space with or without instruction, or where individual and group sporting, athletic and physical activities are participated in competitively or recreationally.

41. Local Authorities may use the following criteria to assess whether a business is eligible for a grant under this threshold:

- Businesses that offer in-person exercise and sport activities to the general public.

Businesses that open to members of the public paying an entry or membership fee.

• Businesses that require extensive cleaning protocols, which significantly slow down trade.

• Businesses that offer exercise classes or activities, which may mandate space and no masks etc.

42. For these purposes, the definition of a gym & sport business should exclude: home gyms, home exercise studios, home sports courts and home sports grounds.

Personal care

43. For the purposes of this scheme, a personal care business can be defined as a business which provides a service, treatment or activity for the purposes of personal beauty, hair, grooming, body care and aesthetics, and wellbeing.

44. Local Authorities may use the following criteria to assess whether a business is eligible for a grant under this threshold:

- Businesses that deliver in-person holistic, beauty and hair treatments.

- Businesses that provide services such as tattoos and piercings.

- Businesses that offer close-contact services, which are required to deliver the treatment.

- Businesses that offer services, treatments or activities that require social distancing and cleaning protocols, which have led to a reduction in their capacity to deliver personal care services.

45. For these purposes, the definition of a personal care business should exclude: businesses that only provide personal care goods, rather than services; businesses used solely as training centres for staff, apprentices and others; businesses providing dental services, opticians, audiology services, chiropody, chiropractors, osteopaths and other medical or health services,

including services which incorporate personal care services, treatments required by those with disabilities and services relating to mental health.

Exclusions to Restart Grant funding

46. The proposed exclusions in the list at paragraphs 30, 33, 36, 39, 42 and 45 are not intended to be exhaustive and it will be for Local Authorities to determine those cases where eligibility is unclear. Billing authorities will have a good understanding of the licensed premises in their areas and will be readily able to form a view on eligibility in the majority of cases.

47. Businesses that are not within the ratings system will not be eligible to receive funding under this scheme.

48. Businesses that have already received grant payments that equal the maximum permitted subsidy allowances will not be eligible to receive funding.

49. Businesses that are in administration, insolvent or where a striking-off notice has been made, are not eligible for funding under this scheme.

How will the grant be provided?

50. In line with the eligibility criteria set out in this guidance, Central Government will fully reimburse Local Authorities, in line with this guidance and the grant offer letter sent to Local Authorities, for the cost of the grant (using a grant under

section 31 of the Local Government Act 2003).

51. This funding will be a one-off lump sum payment from 1 April 2021. Local Authorities will be responsible for delivering the funding to eligible businesses.

52. Local Authorities will receive 90% of the estimated grant funding based on an initial Government estimate. When this threshold of funding has been spent, Government will top up funding to Local Authorities if required. To ensure efficiency and a smooth funding delivery process, unnecessary underspend should be avoided where possible.

53. Local Authorities, subject to local eligibility, will receive funding to meet the cost of payments to businesses within the business rates system based on the number of eligible hereditaments.

54. Local Authorities are business rate billing authorities in England. They are responsible for making payments to businesses and will receive funding from Government.

55. As part of their application process for the scheme, all businesses will be required to self-certify that they meet all eligibility criteria.

56. We are committed to meeting the New Burdens costs to Local Authorities for this scheme. A New Burdens assessment will be completed, and funding then provided to authorities.

57. It is expected that Local Authorities will provide local businesses with grant funding as soon as possible from 1 April 2021.

58. The application closure date for this scheme is 30 June 2021 and final payments must be made by 31 July 2021.

59.The Local Authority must call or write to the business, stating that by accepting the grant payment, the business confirms that they are eligible for the grant schemes. This includes where Local Authorities already have bank details for businesses and are in a position to send out funding immediately, or where the Local Authority is sending a cheque to a business.

Will grants be subject to tax?

60.Grant income received by a business is taxable. The Restart Grant will need to be included as income in the tax return of the business.

61.Only businesses that make an overall profit once grant income is included will be

subject to tax.

62.Payments made to businesses before 5 April 2021 will fall into the 2020/21 tax year. Payments after 6 April 2021 will fall into the 2021/22 tax year. Unincorporated businesses will be taxed when they receive the grant income.

Managing the risk of fraud and payments in error

63.The Government will not accept deliberate manipulation and fraud. Any business caught falsifying their records to gain additional grant money will face prosecution and any funding issued will be recovered, as may any grants paid in

error.

64.Local Authorities must continue to ensure the safe administration of grants and that appropriate measures are put in place to mitigate against the increased risks of both fraud and payment error. In this respect, grant administrators should

supplement existing controls with digital tools to support efficient, appropriate and accurate grants awards.

65.For the avoidance of doubt, Local Authorities are required to undertake prepayment checks for all Restart Grant payments. This is a stricter position than that taken for previous COVID-19 business support grant schemes. These

checks are required to be undertaken before any payments are issued to businesses, and can be commenced in advance of 1 April 2021. This requirement is not limited to new applicants and should look at both the company and the company’s bank account.

Company check

66.The Government Grants Management Function have waived the annual fee and made their digital due-diligence tool, Spotlight, available to Local Authorities to support the administration of COVID-19 emergency grants until 30 June 2021.

Use of Spotlight (or an equivalent tool) or enhanced checks to support pre-award due diligence is required.59.The Local Authority must call or write to the business, stating that by accepting the grant payment, the business confirms that they are eligible for the grant schemes. This includes where Local Authorities already have bank details for businesses and are in a position to send out funding immediately, or where the Local Authority is sending a cheque to a business.

Will grants be subject to tax?

60.Grant income received by a business is taxable. The Restart Grant will need to be included as income in the tax return of the business.

61.Only businesses that make an overall profit once grant income is included will be subject to tax.

62.Payments made to businesses before 5 April 2021 will fall into the 2020/21 tax year. Payments after 6 April 2021 will fall into the 2021/22 tax year. Unincorporated businesses will be taxed when they receive the grant income.

Managing the risk of fraud and payments in error

63.The Government will not accept deliberate manipulation and fraud. Any business caught falsifying their records to gain additional grant money will face prosecution and any funding issued will be recovered, as may any grants paid in

error.

64.Local Authorities must continue to ensure the safe administration of grants and that appropriate measures are put in place to mitigate against the increased risks of both fraud and payment error. In this respect, grant administrators should

supplement existing controls with digital tools to support efficient, appropriate and accurate grants awards.

65.For the avoidance of doubt, Local Authorities are required to undertake prepayment checks for all Restart Grant payments. This is a stricter position than that taken for previous COVID-19 business support grant schemes. These

checks are required to be undertaken before any payments are issued to businesses, and can be commenced in advance of 1 April 2021. This requirement is not limited to new applicants and should look at both the company and the company’s bank account.

Company check

66.The Government Grants Management Function have waived the annual fee and made their digital due-diligence tool, Spotlight, available to Local Authorities to support the administration of COVID-19 emergency grants until 30 June 2021. Use of Spotlight (or an equivalent tool) or enhanced checks to support pre-award due diligence is required.

Annex C – Business categorisation for the purposes of grant funding thresholds

Threshold definitions for the purposes of this scheme are restated below:

- Non-essential retail definition: a business that is open to the public and is used mainly or wholly for the purposes of retail sale or hire of goods or services, where the primary purpose of products or services provided are not necessary to the health and well-being of the public.

- Hospitality definition: a business whose main function is to provide a venue for the consumption and sale of food and drink

- Leisure definition: a business that provides opportunities, experiences and facilities, in particular for culture, recreation, entertainment, celebratory events, days and nights out, betting and gaming

- Accommodation definition: a business whose main lodging provision is used for holiday, travel and other purposes.

- Gym & Sport definition: a commercial establishment where physical exercise or training is conducted on an individual basis or group basis, using exercise equipment or open floor space with or without instruction, or where individual and group sporting, athletic and physical activities are participated in competitively or recreationally.

- Personal care definition: a business which provides a service, treatment or activity for the purposes of personal beauty, hair, grooming, body care and aesthetics, and wellbeing.

This table sets out types of businesses that are eligible under the sector thresholds for this scheme. This list is not exhaustive, but indicative of the types of businesses that can be supported under this scheme.